What data union pay means in 2026

A data union is a consumer-owned cooperative that aggregates personal information from its members to license or sell that data as a collective unit. Instead of individuals selling their data piecemeal to third-party brokers, members pool their digital footprint—such as browsing history, location data, or purchase records—into a single entity. This structure allows the union to negotiate licensing agreements with corporations on behalf of all participants, ensuring that the value generated from personal data is returned to the users rather than captured by intermediaries.

The model draws its name from traditional labor unions, but the mechanism of compensation differs significantly. While labor unions negotiate wages and working conditions through collective bargaining agreements, data unions operate on a data-sharing framework. Members contribute their data, and the union distributes the resulting revenue, often in the form of direct payments, platform credits, or improved services. This approach shifts the power dynamic from corporate data extraction to consumer-owned data cooperatives, giving individuals a clearer claim to the economic value of their digital lives.

Legal compliance and transparency are central to the data union model. Unlike opaque data brokerages that often obscure how data is collected and sold, data unions typically operate with clear governance structures and user consent protocols. Members must explicitly opt in to data sharing, and the union is responsible for anonymizing or aggregating data to protect individual privacy while maintaining its commercial value. This focus on consent and regulatory adherence is critical as governments worldwide tighten data protection laws, making compliant data monetization a viable business model for the first time.

In 2026, the distinction between data unions and traditional data brokers is increasingly defined by ownership and distribution. Brokers act as middlemen who buy and resell data without returning value to the source, whereas data unions retain ownership of the aggregated dataset and distribute profits to members. This structural difference addresses long-standing concerns about data exploitation, offering a transparent alternative where users are compensated for the data they generate.

Comparing top data union platforms

The landscape of Web3 data monetization is defined by three primary mechanisms: stablecoin payouts, native token rewards, and revenue-sharing models. For legal and regulatory audiences, the distinction between these models is not merely financial but determines the classification of the asset and the compliance burden on the platform. Stablecoin payments (USDC, USDT) generally align with traditional contractor compensation, while token-based rewards introduce securities law considerations depending on the token's utility and governance rights.

The following comparison outlines the mechanics of leading data union platforms. These entities vary significantly in the types of data they collect, ranging from passive internet traffic logs to active survey responses, and in their privacy guarantees, which often involve zero-knowledge proofs or differential privacy techniques to anonymize contributors before aggregation.

| Platform | Payout Mechanism | Primary Data Type | Min. Withdrawal |

|---|---|---|---|

| Ocean Protocol | OCEAN Token | Datasets & AI Models | Variable |

| Hivemapper | HONEY (Stablecoin) | Dashcam Mapping | $10.00 |

| Brave Rewards | BAT (Token) | Ad Attention | $1.00 |

| Covalent | CQT Token | Blockchain Data | Variable |

Payout Currency and Legal Classification Platforms paying in stablecoins (like Hivemapper’s HONEY) often face fewer regulatory hurdles regarding securities laws, as the payout is pegged to fiat value and functions similarly to a service fee. Conversely, platforms paying in native tokens (Ocean, Brave, Covalent) must plan around the Howey Test more carefully. If the token is deemed an investment contract, the platform may be required to register with the SEC or comply with state-level money transmitter laws. Contributors should review the platform’s Terms of Service to understand if the payout token is classified as a utility token or a security.

Data Types and Privacy Guarantees The value of the data collected dictates the payout rate. Blockchain data (Covalent) is highly structured and valuable for indexing, often requiring minimal user effort. In contrast, mapping data (Hivemapper) requires physical movement and hardware, creating a higher barrier to entry but potentially higher per-mile rewards. Privacy is maintained through aggregation; individual data points are rarely sold. Instead, unions sell aggregated datasets to enterprises. Users should verify if the platform uses zero-knowledge proofs (ZKPs) to ensure that their personal identity cannot be linked to their data contributions.

Minimum Withdrawal Thresholds Withdrawal limits vary widely. Platforms with low thresholds (under $10) facilitate micro-transactions but may incur high gas fees on Ethereum or other congested networks. Some platforms allow withdrawals only after reaching a specific token balance, which can be a barrier for casual users. Always check the network fees associated with the withdrawal method, as these can significantly erode small payouts.

Stablecoin Payouts and Tax Implications

Data unions primarily distribute earnings in stablecoins such as USDC or USDT to facilitate global, low-friction payments. While this mechanism allows for rapid settlement and borderless access, it introduces significant regulatory complexity. For participants in the United States, these transactions are not merely digital transfers; they are taxable events that require strict adherence to Internal Revenue Service (IRS) guidelines.

How Stablecoin Payments Work

When you contribute data to a union, the platform converts your contribution into a credit balance. Payouts are typically issued in stablecoins pegged to the US dollar, minimizing volatility compared to other cryptocurrencies. You receive these funds directly into a compatible self-custody wallet or a supported exchange account.

This process is automated and transparent. The smart contract executing the payout records the transaction on the blockchain. However, the blockchain record alone does not satisfy tax reporting requirements. You must track the fair market value of the stablecoin at the moment of receipt. Even though the value is stable, the IRS treats stablecoins as property, not currency. This distinction is critical for accurate reporting.

Tax Reporting Requirements

The IRS requires you to report stablecoin income as ordinary income on the date you receive it. This applies whether the funds are withdrawn to a bank account or held in your wallet. If you use the stablecoins for goods or services, or if you trade them for another cryptocurrency, you trigger a capital gains or loss event.

Failure to report this income can result in penalties and interest. The high-stakes nature of compliance means you must maintain detailed records of every transaction. This includes the date, time, USD value, and the purpose of each transaction. Relying on the platform’s payout history is a good start, but it may not capture all taxable events, such as staking rewards or governance token distributions.

Record Keeping Best Practices

To meet these requirements, use tax software that supports cryptocurrency tracking. Import your wallet transaction history and reconcile it with the data union’s payout records. Be aware that some platforms provide tax reports, but they may not be comprehensive. Cross-referencing these reports with your on-chain activity is essential for accuracy.

As regulatory frameworks evolve, staying informed about changes in tax law is vital. The landscape for digital asset taxation is dynamic, and what applies today may change tomorrow. Proactive management of your records ensures you remain compliant and avoids costly surprises during tax season.

Privacy risks in decentralized data markets

Participating in Web3 data unions involves a fundamental tradeoff: exchanging personal information for compensation while attempting to maintain anonymity. Unlike traditional employment where wages are paid in fiat currency, data monetization platforms often operate on public ledgers, making the link between a contributor’s identity and their earnings potentially visible to third parties. This transparency creates unique privacy vulnerabilities that traditional labor models do not face.

Reputable data union platforms mitigate these risks through advanced cryptographic techniques rather than simple pseudonymity. Zero-knowledge proofs (ZKPs) allow contributors to verify their eligibility or the validity of their data without revealing the underlying personal details. For instance, a platform might prove that a user is over a certain age or resides in a specific jurisdiction without disclosing their exact birthdate or address. This approach ensures compliance with data collection requirements while minimizing the exposure of sensitive personal information.

Anonymization remains the primary defense against de-anonymization attacks, where adversaries attempt to re-identify individuals by correlating dataset entries with external public records. Leading platforms employ differential privacy, adding statistical noise to datasets to prevent the identification of any single individual. However, legal experts note that as datasets grow larger and more interconnected, the risk of re-identification increases. Contributors must understand that while their data is anonymized, the aggregation of multiple data points can sometimes reveal patterns that compromise individual privacy.

Regulatory frameworks like the GDPR and CCPA impose strict obligations on data controllers, including those in the decentralized space. Platforms that fail to implement robust privacy-preserving measures may face significant legal liability. Contributors should review the privacy policies of any data union they join, paying close attention to how data is stored, processed, and potentially shared with third-party analytics firms. The financial reward must be weighed against the long-term implications of having one’s digital footprint recorded on a blockchain.

Is data union pay right for you

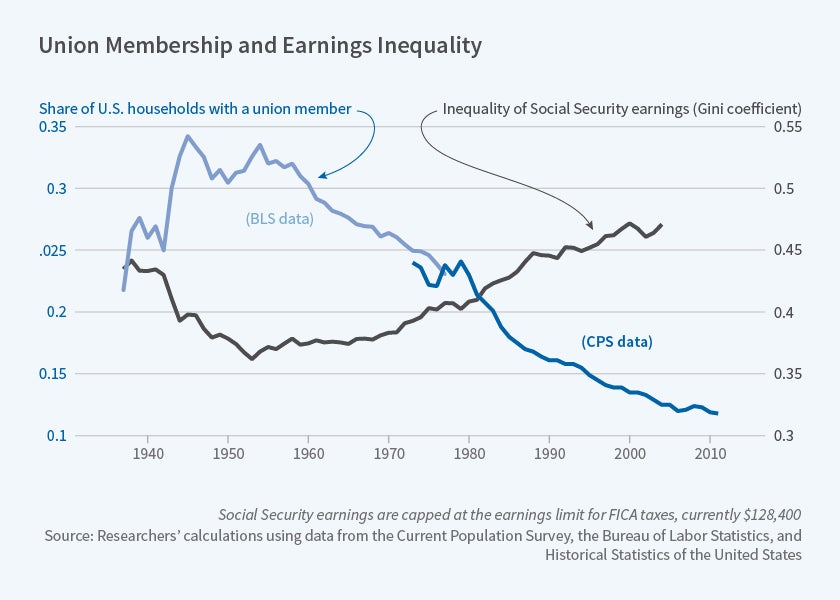

Data union pay models operate on a different premise than traditional labor organizing. While the Bureau of Labor Statistics reports 14.7 million union members in 2025, these Web3 data cooperatives do not negotiate wages or collective bargaining agreements [1]. Instead, they aggregate user data to generate revenue, distributing payouts directly to participants. Understanding this distinction is essential for evaluating whether the model aligns with your privacy standards and income expectations.

The financial reality of data union participation is modest. Most platforms operate as secondary income streams rather than primary employment. Payouts depend on data volume, quality, and market demand for specific datasets. Unlike the 11.2% wage premium often cited for traditional union members [2], data union rewards are variable and rarely replace earned income. Participants should view these earnings as incidental rather than reliable compensation.

Privacy compliance remains the primary consideration. Legitimate data unions adhere to GDPR and CCPA frameworks, ensuring data is anonymized before sale. However, the technical complexity of true anonymization varies by platform. If your priority is maximizing income over privacy control, traditional employment offers more predictable returns. Data union pay suits those willing to trade minor data points for small, passive returns while maintaining strict oversight of their digital footprint.

No comments yet. Be the first to share your thoughts!